- Details

- Written by Dr. Duke

- Category: Dr. Duke's Blog

- Hits: 1836

I was surprised to see SPX and RUT move in opposite directions today. SPX closed lower by $4 at $2040, but RUT actually traded higher, closing at $1216, up $7. The VIX increased by a couple of tenths to 16.9%, so there wasn't much change there. Trading volume fell on all fronts, with 2.1 billion shares of the S&P 500 stocks trading today, below the 50 dma of 2.2B. Trading volume declined 7% on the NYSE and declined 3% on NASDAQ.

There wasn't any significant economic data issued today, but we will get both retail sales and the weekly unemployment numbers tomorrow. A solid retail sales number could calm this market, but recent retail sales data have been weak.

Perhaps this mixture of a lower SPX with a higher RUT suggests an equilibrium being reached? If so, maybe we are back into the sideways trading range from January. But a weak retail sales number tomorrow could easily push us lower to test that 200 dma on SPX around $2002.

My March condor on RUT stands at a net gain of 6.2%; the delta of the short 1160 put is 8 today. It is borderline whether we will close the put spreads Friday with the Two Sigma Rule. If volatility expands, we will be closing the March put spreads; if not, we may be able to safely leave them open through the weekend.

- Details

- Written by Dr. Duke

- Category: Dr. Duke's Blog

- Hits: 2014

That jab in the nose hurt! SPX dropped $35 or 1.7% to close at $2044. SPX didn't even hesitate at the 50 dma at $2061. RUT lost $15 or 1.2% today, closing at $1208. $1210 was the high reached twice in 2014 by RUT and that level also served as resistance in early February before RUT took off to set new all-time highs. RUT's 50 dma is at $1203, but this market may give back more than that before it is done. Volatility is starting to heat up, with the VIX gaining 1.6 points today to close at $16.7%. That places us back in the range of volatility from the choppiness we endured in January.

Conventional technical analysis would conclude from today's price action that we are now back in that choppy range from January, roughly $1990 to $2065. The 200 dma is at $2001, just above that support level at $1900. Today's price takes us down 3.4% from the high on March 2nd. If you follow Fibonacci retracements, the 62% retracement level is at $2034 on SPX. I have not used Fibonacci much myself, but I have been surprised how often those numbers seem to arise. That $2034 level would be a 4% correction, similar to what we saw in mid-December and early January. In any case, all one can do is mark some points where positions must be adjusted or closed, watch what the market gives us each day, and take appropriate action.

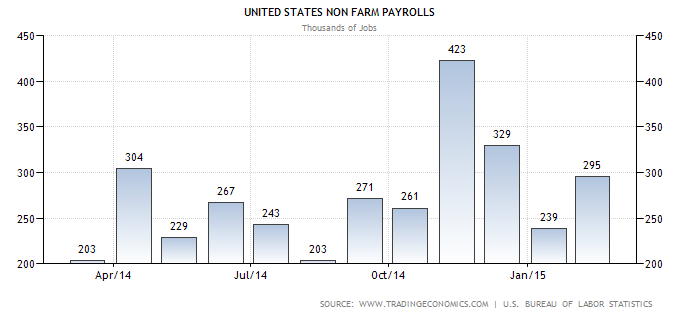

The conventional wisdom for this correction appears to be the "unusually good" jobs report causing traders to expect increased interest rates from the Fed sooner than expected. I explained why I thought that unlikely yesterday, but I found a nice graphic illustrating the problem. In the chart below of the non-farm payroll numbers for the past 12 months, it is hard to see the February number as "unusually good". In fact, it's hard to identify a trend. But I received that headline on my phone from Yahoo Finance as the explanation for this market pull back, so it must be true.

My March iron condor position on RUT stands at a net gain of 2% (increased implied volatility pulled it back), and delta for the position equals +$57 and position theta = +$229. Delta of the short $1060 puts = 12, so we are pretty safe at this point. We will hit our two sigma rule Friday, so we may be closing the put spreads then if not before. The April condor is delta neutral (position delta = +$19 on 20 contracts) and is showing a small gain of 1% at this point. Hold on for the ride!

- Details

- Written by Dr. Duke

- Category: Dr. Duke's Blog

- Hits: 1713

Traders continue to tread water with an eye toward Friday's jobs report. SPX closed down $9 at $2099, and RUT traded down $4 to $1231. SPX opened lower this morning and traded down to $2088 before bouncing around 11 am ET, and then traded sideways the rest of the day. Both today and yesterday's intraday lows strengthen the support level of $2090 on SPX. Also note the long lower shadows on yesterday and today's candlesticks - another indication that the bulls remain in control.

Traders were concerned about the market's reaction to the Beige Book (FOMC minutes from the last meeting). As it turned out, there was no reaction whatsoever. Trading volume continued to be flat with two billion shares of the S&P 500 trading. Trading volume on the NYSE rose 3%, but declined 8% on NASDAQ. Volatility rose a bit both yesterday and today, with the VIX closing at 14.3%.

The ISM services index came in at 56.9 for February, about even with last month's 56.7. ADP reported their private payroll number for February at 212 thousand jobs, down from January's 250 thousand. Does that foretell a weak jobs report Friday? Perhaps, but the correlation has been tenuous historically. But it will cause traders to stay on the sidelines until after the jobs report. The only probable activity tomorrow will be to take some vulnerable profits off the table.

- Details

- Written by Dr. Duke

- Category: Dr. Duke's Blog

- Hits: 1808

After all of the doomsday prophets on Friday, one had to wonder what might happen today. One day doesn't make or break a trend, but today's market action was encouraging. SPX traded as high as $2083 before settling back at $2079 for a gain of $8. RUT followed suit with a gain of $6, closing at $1224. Volatility was basically unchanged with the VIX closing down a tenth of a point to 15.1%. Trading volume was down from Friday's high numbers, with two billion shares of the S&P 500 stocks trading; the 50 dma is 2.2B. Trading volume dropped 16% on the NYSE and decreased 11% on NASDAQ.

Friday's sell-off was sufficient to push IBD to move from "Confirmed Uptrend" to "Uptrend Under Pressure". Watch their web site this evening to see if that moves to "Market in Correction" - probably not after today's small gains.

There was no economic news today, but I looked up the non-farm payroll data for the past twelve months. The conventional wisdom for Friday's sell-off was something to the effect that such an "unusually good" jobs report would cause the Feds to increase interest rates in June rather than September. When I look at the data, it is pretty choppy and I fail to see February's 295k as "unusually strong". We had 304k back in May of last year and 423k in November. The only thing positive about the February number is that it saved us from drawing a downward trend line from November through February (December was 329k and January reported 239k). I'm not convinced this is the definitive "last word" for Yellen's assessment of the economy. For now, remaining bullish appears to be the safer alternative. Whenever interest rates begin to rise, it will slow the economy, and that is precisely why I think the FOMC will be slow to take that step when we are still observing mixed data.

- Details

- Written by Dr. Duke

- Category: Dr. Duke's Blog

- Hits: 1877

Just when it seemed that the bulls might be taking a rest, they come roaring back. SPX gained $13 to close at $2117 and RUT closed at $1243, up $9. Volatility continues to contract with the VIX dropping about a third of a point to 13.0%. Trading volume remains anemic with 2.1 billion shares of the S&P 500 trading. Trading was up 2% on the NYSE and up less than one percent on NASDAQ.

Over 90% of the S&P 500 companies have reported fourth quarter earnings at this point and about 75% have beat the analysts' earnings estimates. Concern about the strong dollar hurting the earnings of the multinationals appears to have been overblown. The Greek debt problem is certainly not solved, but traders seem to have moved on.

The pattern appears to be: 1) the bulls push higher, 2) bears present a "sky is falling" scenario, 3) markets trade sideways while we worry, and then 4) the bulls push higher.

Will Friday's jobs report be the next focus of worry?